Most people don’t start thinking about taxes until January rolls around. But if you’re an entrepreneur, you have so much more to keep up with than the average person. Self-employment taxes. Employee taxes. Quarterly estimated taxes. It’s a lot. Figuring out how to effectively manage your tax situation should always be on the brain.

With that in mind, here are five quick ways to manage and reduce taxes as an entrepreneur. (And heads up — if you’re a high-income-earning entrepreneur making over $250,000 a year, we have more advanced strategies for you at the end of this article.)

1. Save For Retirement

Putting money into a retirement account throughout the year has two benefits: you build wealth for the future and you lower your taxable income for the current year. It’s a double win.

For example, let’s say you made $200,000 this year and saved $50,000 of that for retirement. When you filed your taxes, only $150,000 would be considered taxable by the IRS.

The maximum amount you can contribute to a traditional or Roth 401(k) in 2021 is $6,000, plus an additional $1,000 if you’re at least age 50. (1) (Although, fair warning, contributing to a Roth IRA doesn’t lower your taxable income now. Those benefits come later when you retire.)

Because you’re self-employed, you also get access to other retirement accounts not available to the general public. For example, you can open a SEP IRA and save as much as 25% of your income (up to $58,000). (2) You may also have the option to open a solo 401(k), which allows you to contribute even more.

2. Choose The Right Business Structure

Your business structure determines the types of taxes you pay, how much paperwork you have to fill out, and your personal liabilities.

Most entrepreneurs start out as a sole proprietor or LLC, where they’re fully responsible for everything, then switch over to a corporation as their company grows and becomes more profitable.

As with most things in life, there is no one-size-fits-all business structure. It’s important to talk to a wealth advisor and CPA to see which structure makes the most sense for your business.

3. Keep Track Of Deductions

It’s easy to forget about all the expenses you made throughout the year when you’re laser-focused on growing your business. But it’s important to document as much as you can throughout the year so you can take advantage of every deduction and credit you qualify for.

If you’re using a good bookkeeping system, it should be fairly easy to keep up with your income and expenses. Platforms like QuickBooks Self-Employed even categorize your expenses into a Schedule C form, so you can simply review and export it when it’s time to file your taxes.

There are dozens of expenses you can deduct as an entrepreneur. (3) Here are a few common ones:

- Startup costs

- Advertising

- Bank, legal, and professional fees

- Fees for online services and subscriptions

- Travel expenses

- Charitable contributions

- Education, research, and development expenses

- Software, hardware, and other equipment

- Health insurance premiums and medical care expenses

- Home office and supplies

- Inventory

- Repairs, maintenance, and utilities

- Retirement contributions

- Contract employees

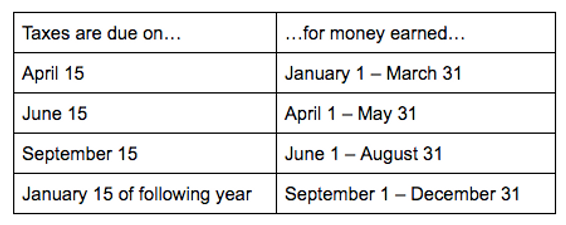

4. Pay Quarterly Estimated Taxes On Time

When you’re self-employed, you’re responsible for paying your own taxes to the IRS in the form of quarterly estimated payments. They’re not automatically taken out of your paycheck for you as they are with W-2 employees.

This table highlights when quarterly estimated payments are typically due: (4)

You may pay penalties and fees if you don’t pay the IRS what is owed to them, so it’s critical to stay on top of these dates.

Most entrepreneurs set aside at least 30% of their income for taxes, but this isn’t a hard-and-fast rule. The exact amount you’ll need to set aside depends on your business structure, tax bracket, state of residency, and more.

A wealth advisor can take a closer look at your situation and help you figure out exactly how much you should pay each quarter.

5. Don’t Go At It Alone

These are just a small handful of fundamental tax mitigation strategies we use with our clients. We also have many advanced strategies for our high-income-earning-entrepreneurs making more than $250,000 a year and wanting to save more than $50,000 a year for their future.

Some of these strategies include:

- Money purchase pensions

- Premium financing

- Business entities such as insurance captives

About John

John Halterman, best-selling author and nationally published blogger has been featured as a financial guest expert on the TV shows of self-help gurus Brian Tracy and Jack Canfield, author of Chicken Soup for the Soul. He has appeared on ABC, FOX, BRAVO, NBC, CBS, and A&E. John is the expert host of the weekly WDTV News 5 segment, “Solutions 4 Financial Independence.”

As an authority on wealth management, he has been invited by hundreds of institutions such as universities, federal agencies, professional associations, and large energy and utility corporations to be a guest speaker and educational event host. Event topics include maximizing your retirement, managing down market investment risk, how to reduce your tax burden, and transferring your family wealth in the most tax advantageous way.

John is the founder and owner of Beacon Wealth Management, specializing in helping entrepreneurs, professional practitioners, and retirees overcome the 4 major challenges facing successful families. He is a warm communicator with a passion for helping people transform their financial futures. John understands the multifaceted set of financial worries people face as they become more successful and enter the retirement red zone. He empathizes personally with each client and delivers a collaborative client experience that empowers people to reach their life goals.

With more than two decades of experience, John’s professional credentials include:

- Certified Wealth Strategist (CWS)

- Accredited Investment Fiduciary® (AIF®)

- Certified Estate Planner™ (CEP®)

- Chartered Federal Employee Benefits Consultant℠ (ChFEBC℠)

- Professional Plan Consultant® (PPC®)

- Registered Financial Consultant (RFC)

- Past member of Ed Slott’s Master Elite IRA Study Group

A native of Weston, West Virginia, John served in the United States Air Force prior to becoming a Wealth Advisor. Today, he resides with his family in Bridgeport, West Virginia. He and his wife, Lisa, have been married since 2005 and have three amazing children. A family-loving man, he enjoys giving back to his community, coaching youth sports, landscaping and architectural design, WV Athletics, and is an outdoor and racquetball playing enthusiast.

_____________

(3) https://www.entrepreneur.com/article/219474

(4) https://www.irs.gov/faqs/estimated-tax/individuals/individuals-2